Housing shortage seeds planted years ago

Key Takeaways

Somewhere in your county, a job is sitting empty simply because the person who would take it can’t find a place to live. They might be a teacher, a nurse, a deputy or a kid who grew up there and would love to move back — if only the math made sense.

The local loss now felt nationally is partly downstream of a housing supply shortage that began decades ago in America’s priciest coastal markets, where layers of well-meaning land-use regulation gradually constrained new construction, even as big cities added millions of high-paying white-collar jobs.

Starting in the late 1980s and picking up steam in the 2000s, a small cluster of “superstar cities” began accounting for an increasingly large share of America’s job growth. High-skill service industries (finance, law, media, tech) increasingly concentrated in New York, San Francisco, Boston, Seattle, Los Angeles and Washington, D.C., increasing incomes for workers in these markets even as housing supply remained fixed.

With housing supply effectively capped by zoning in America’s fastest-growing job markets and no more land to develop within commuting distance of job centers, prices did what prices do: increased dramatically in the face of fixed supply and increased demand. The Federal Reserve Bank of Dallas estimates that underbuilding since the start of the 21st century raised home prices about 20% relative to incomes, breaking a link that had held for 50 years.

The housing constraints in these places were not always inevitable. For much of the mid-20th century, many Americans moved outward from city centers into newly built suburbs, creating room for metropolitan growth to continue. But as younger professionals and high-skill industries began moving back into urban cores in the late 20th century, those same markets reached the limits of the old growth model. In places like New York, San Francisco and Los Angeles, geography made outward expansion increasingly difficult: oceans, mountains, long distances and limited developable land constrained the traditional suburban response.

At the same time, the country was responding to real failures of the postwar development model. The destruction of established neighborhoods through urban renewal, highway construction and growing concerns about pollution and environmental damage — produced a bipartisan push in the 1970s for stronger environmental protections and more community input. Those reforms addressed legitimate problems, but over time, some approval processes created additional delays, uncertainty and opportunities for opposition even for projects with limited environmental impacts.

People priced out did the rational thing and left their expensive hometowns — heading to Austin, Phoenix, Nashville and the small towns and exurban counties an hour past them that were willing to accommodate population growth. The Sunbelt built furiously and still couldn’t keep up, because it was absorbing a problem it hadn’t created.

With the rise of remote work, another wave of highly paid professionals moved out of high-cost markets and into smaller metros, exurbs and rural communities — further bidding up the price of housing nationwide. The South now carries the largest accumulated deficit of housing units of any region while building more than any other. This seeming paradox is what it looks like to inherit someone else’s problem. Had the high-cost, mostly coastal markets added homes at Sunbelt rates, the country would have several million more homes and lower prices across the board.

Since this problem became apparent, local governments have started to solve it. Reform came at every level. Minneapolis ended single-family zoning in its 2040 plan; Austin paired upzoning with permitting reform. Austin added roughly 120,000 homes from 2015 to 2024 — a 30% jump against 9% nationally — and rents fell about 20% from their 2022 peak. Minneapolis grew its housing stock 12% while rents rose 1%, even as the rest of the state watched rents climb by 14%.

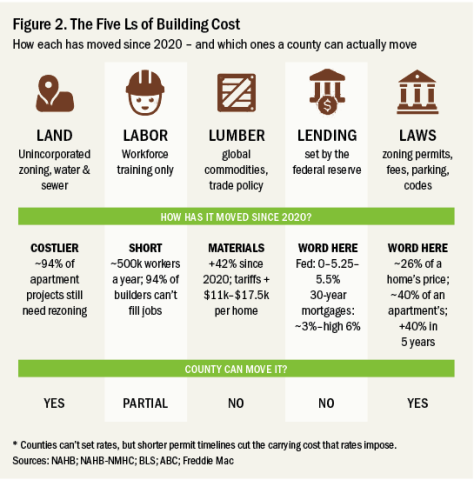

Over the past 15 years, as interest in land use and housing affordability has increased and a wave of localities have passed zoning and regulatory changes to allow more housing, the issue has only gotten worse. So why are national starts stuck and prices still climbing despite the best efforts of local reformers? Because reform ran headlong into a wall of cost, and the timing was almost comically bad. Builders sort the cost drivers of new housing into five Ls — land, labor, lumber (materials), lending and laws. Reform loosened the constraints imposed by laws and land-use rules while lending, labor and lumber all moved the wrong way at once.

Lending hit hardest: after the Federal Reserve lifted interest rates past 5% in 2022 from near zero, projects stopped “penciling” — a deal pencils only when expected rents cover land, construction and financing with enough left to repay the banks and funds that fronted the money, and those investors weigh every deal against safe Treasury bonds.

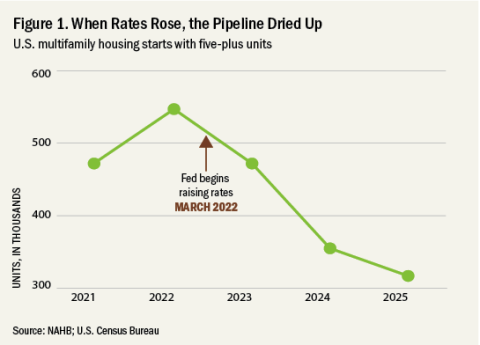

When risk-free Treasury bonds offer returns above 5%, investors demand higher returns from riskier real estate projects, causing many developments to fail underwriting. Multifamily starts fell toward an estimated 317,000 in 2025 from about 547,000 in 2022 (Figure 1). You can watch it happen permit by permit — Washington, D.C. apartment permits dropped to two per thousand residents from roughly 11 per thousand residents. Reform opened the door to new construction at almost the precise moment financing for it vanished.

The rest piled on: American material costs have increased roughly 40% since COVID-19, while tariffs and a persistent construction labor shortage have driven construction labor costs even higher.

Put it together and a once-in-a-generation cost shock canceled out the would-be positive effects of land-use reform. With most owners holding sub-6% mortgages, the resale market froze on top of it.

This is where counties come in. Three of the five Ls sit above the county pay grade: no county sets interest rates, trade policy or immigration law. But land and laws — the two reform targets — are exactly what states hand to local government, and the least-used piece of that authority is unincorporated land. The levers are concrete and cheap: permit timelines (review now adds about seven months to construction timelines, and every month trimmed quietly erases carrying cost), impact and utility fees (close to 9% of an apartment’s cost), the building code, parking rules, and — through water and sewer — whether a parcel can be built on at all.

For counties with the financial capacity to intervene directly in capital markets, there is an additional maneuver to solve the lending freeze: replacing the missing private money.

What that looks like varies widely. Montgomery County legalized small apartment buildings along its corridors and fast-tracked office-to-housing conversions; Miami-Dade County, Fla. waived impact fees for workforce housing across its unincorporated areas and Montana streamlined the subdivision review its own builders called the bottleneck. In each case, different governments with very different budgets found the “L” they controlled and made it cost less. None of this is a magic wand, and the reform wave hasn’t gone far or fast enough to outrun what rates and tariffs did to it. But rates won’t stay high forever, and when the money returns, building resumes first where the land was already zoned for it and the rules weren’t fighting it.

Related News

Counties get creative with land use to add affordable housing

Orange County, Fla. is working to develop affordable housing on land owned by religious institutions and Fairfax County, Va. is exploring co-locating its libraries with affordable housing.

Landmark housing reform bill becomes law with key county priorities

The latest version reflects several NACo advocacy priorities, including increased safeguards for critical community development funding and an expedited process for allocating disaster recovery funds.

County invests in emerging developers to ease housing crunch

Shelby County, Tenn. offered instruction, connections and mentorship to budding real estate developers to bring fresh ideas and approaches to the market.

County News

Housing shortage bedevils public lands counties, employers, feds

Restrictions on how the federal government can pay for housing for employees has prompted the U.S. Forest Service to work with a county to develop residential units, thanks to a farm bill provision.