Affordable Housing: Toolkit for Counties

Upcoming Events

Related News

Introduction

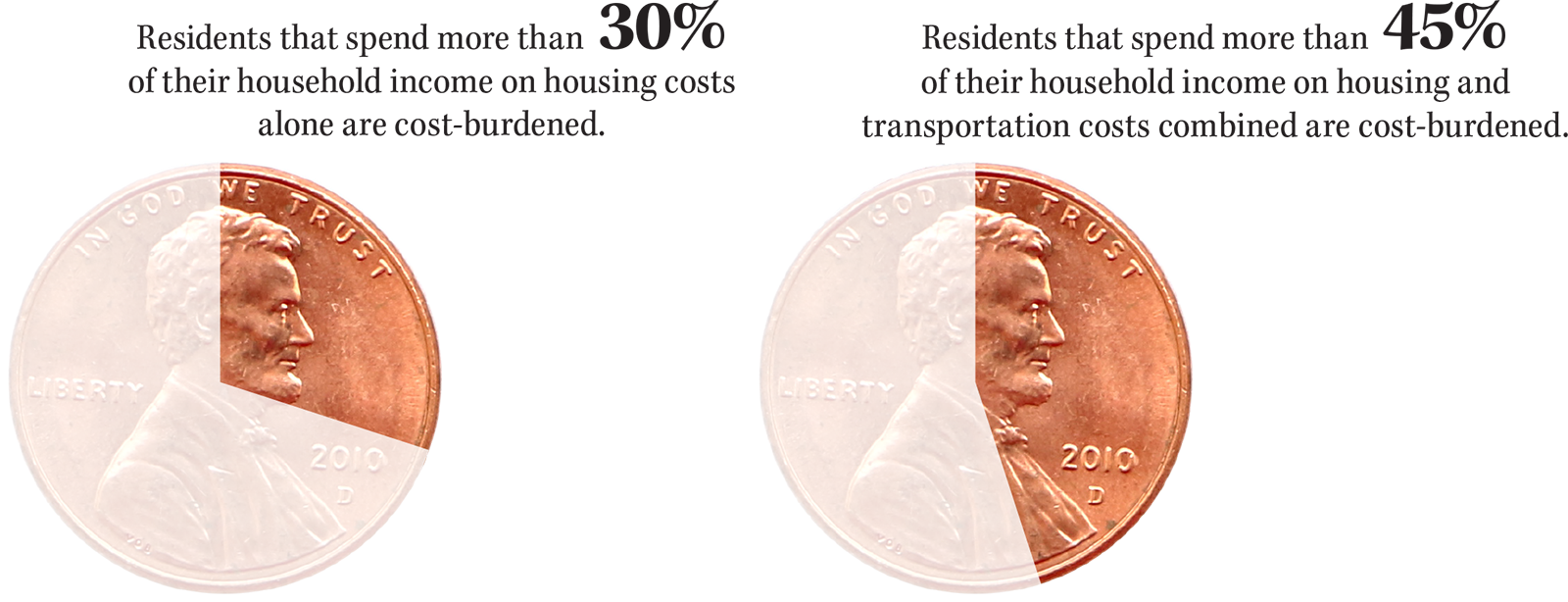

Counties of all sizes and in all regions of the country are struggling with housing affordability. In 2016, over one-third of all American households (34 percent) were burdened by housing costs, in that they spent more than 30 percent of their income on housing.1 This challenge is most pronounced in large counties, where 34 percent of homeowners with mortgages and 53 percent of renters were burdened by housing costs in 2016.2 That said, medium-sized and small counties are also struggling with housing cost burdens: half of renters in medium-sized counties, 46 percent of renters in small counties and 28 percent of homeowners with mortgages in both categories had housing costs that exceeded 30 percent of their household income.3

Although housing affordability affects counties of all sizes in every region of the U.S.,4 each county is unique, facing its own set of obstacles and equipped with its own set of tools to navigate these obstacles. This toolkit, therefore, outlines the role of counties in addressing housing affordability, the extent of the problem and a variety of county-level solutions in four major categories: (1) inter-jurisdictional partnerships; (2) funding and financing solutions; (3) planning and zoning strategies; and (4) federal resources. Finally, the toolkit includes an appendix, which discusses common housing affordability metrics, reviewing their characteristics and limitations. This toolkit summarizes and builds on research conducted by the NACo Counties Futures Lab throughout 2018.

Affordability Measures

The U.S. Department of Housing and Urban Development (HUD) categorizes households relative to the area median income (AMI) to determine whether they qualify for housing programs:

Constituents in communities nationwide are calling on county elected officials to reduce the burdens of housing costs that force residents to relocate to more affordable neighborhoods. Although housing affordability is a shared priority across the country, available options to promote affordability vary widely between counties due to differences in jurisdiction and authority under state constitutions and statutes.

Funding Sources

State law can sometimes proscribe the entities that have budgeting authority within a county; therefore, the funding streams that are available and the process for approving funding varies for counties operating in different states.5 Counties are controlled by state requirements regarding allowable property taxes, debt limits, bond issuance, special districts and more. For example, the State of Alabama enacted rules on timelines for county budgeting, budget creation and adoption procedures and a requirement that revenues cannot exceed expenditures.6

Zoning and Land Use

Counties deploy a broad range of zoning strategies to increase the housing stock as permitted under state laws.7 Counties also have varying degrees in authority to acquire, hold and sell public land.8 State laws outline planning, land use and zoning authority to provide direction to county governments on permissible types of regulations, such as mixed-use zoning, which is not allowed in every state.9 In Pennsylvania, county governments enjoy broad authority over planning and zoning, for state law gives county officials authority over county and public lands.10 In New York, however, county officials only have authority over county-owned properties.11

Partnerships and Interlocal Agreements

Since counties do not often have the resources they need to meet the growing demand for affordable housing, many have developed interlocal agreements with other counties, municipalities, developers and other organizations. State laws also provide guidelines for counties seeking to enter into these types of agreements.12 For example, contracts made by Nebraska counties are under the Inter-local Cooperation Act, which stipulates that the county board may not enter into another contract if the cost of leased equipment or property exceeds one tenth of the county’s total value of taxable property.13

County Operations

Housing affordability is increasingly impacting central county operations. Recruiting and retaining employees is more difficult for counties without affordable housing options, leading many workers to seek employment in more affordable areas.14 Engaging the community on proposed developments and programs has become increasingly important as jurisdictions weigh competing priorities in resource allocation and land use decisions.15 Finally, as the issue of housing affordability has come to the fore, access to data to help design and evaluate community-specific programs has become an imperative.

Download the Full Toolkit

Download the full toolkit and access best practices and analysis.

Resource

Advancing Local Housing Affordability: NACo Housing Task Force Final Report

NACo endorses bipartisan legislation to help volunteer first responders access affordable housing

On June 10, Sens. Tammy Baldwin (D-Wis.) and Kevin Cramer (R-N.D.) reintroduced the Volunteer First Responder Housing Act (S.4737), bipartisan legislation that would help qualified volunteer first responders access affordable housing.

House passes revised housing package with key county wins

House passes revised 21st Century ROAD to Housing Act, reflecting key feedback offered by counties.

NACo endorses bill to support, finance transit-oriented development projects

On April 20, NACo endorsed the Build Housing, Unlock Benefits and Services (Build HUBS) Act (H.R. 7062/S. 3636).