Financial Services News - Nov. 30, 2015

Upcoming Events

Related News

Rising Rates Likely to Impact County Finances

Rock-bottom interest rates and easy money may be coming to an end, as the Federal Reserve prepares to hike rates as early as next month.

Long-term interest rates have remained historically low for an unprecedented stretch of time. Take a look at the 10-year Treasury rate, typically considered the standard reflection of a risk-free rate of return.

After rarely dipping below 4 percent over the prior five decades, rates plunged to 2.5 percent during the financial crisis. Now, six years into the recovery, the rate remains stuck in a narrow range just under 2.5 percent. Likewise, the effective federal funds rate which indirectly influences debt pricing nationally, rapidly dropped to near zero in late 2008 in the midst of the financial meltdown. For seven years, it has barely budged.

Unemployment Trending Down

Employment growth remains subdued compared to past recoveries; however, persistent jobs growth combined with a shrinking labor force participation rate has driven the unemployment rate down to near 5 percent — a level considered close to full employment by many economists. Meanwhile, economic growth has also been quite tepid compared to other post-WWII recoveries, hovering close to 2 percent annually; yet, this too has been of a prolonged, steady nature.

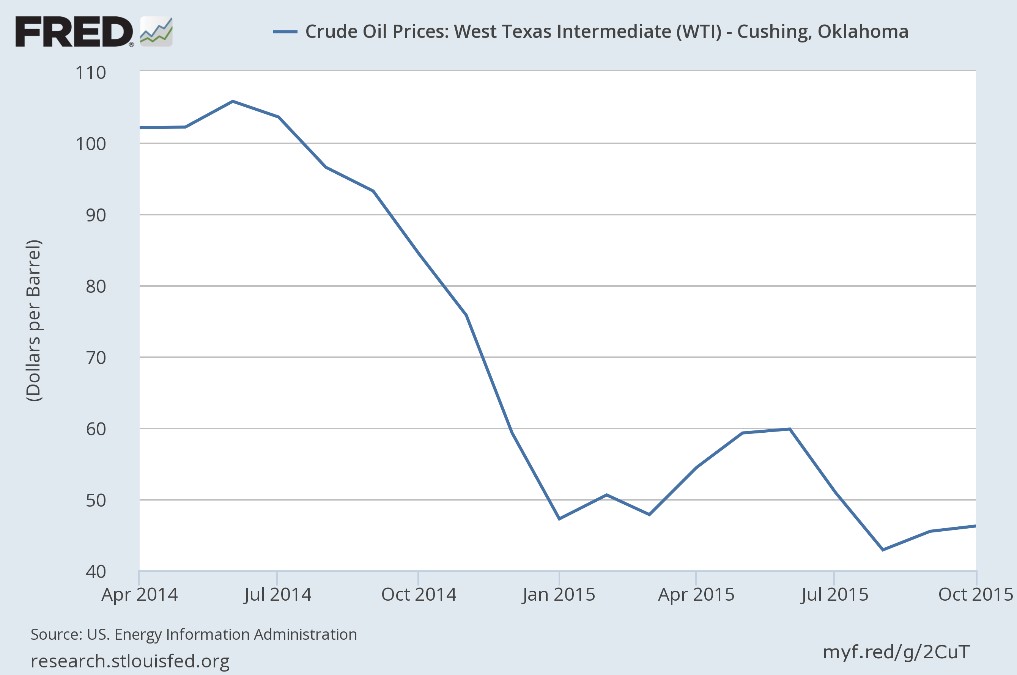

With dramatically lower energy prices potentially bottoming, any increases in other production inputs may quickly ripple throughout the broader economy. Indeed, the recent uptick in real wage growth (2.7 percent over past 12 months) suggests this period of steady growth, cheap money and ultra-low inflation could be coming to an end. As such, the Federal Reserve needs to get in front of any inflationary pressures before it gets out of control.

LOCAL GOVERNMENT DEBT CHART

Local Governments Benefit

This policy change will impact local government budgets for numerous reasons.

Perhaps most importantly, state and local governments have taken advantage of these low rates. Total liabilities (excluding employee retirement funds) nearly doubled from $1.6 trillion in late 2003 to more than $3 trillion in 2010 before leveling off. Interest payments on this debt could dramatically increase as debt is refinanced — particularly if the initial debt were financed with short-term loans. Prudence suggests officials lock in this debt at the current low long-term rates before the increase.

Interest Rates Likely to Rise

For many local governments, the powerful bull market has replenished defined-benefit pension funds. This market has also inflated price-to-earning ratios in many sectors. As earnings cool and debt becomes more attractive as an investment, equities markets will possibly generate far more tame returns. In fact, the broad U.S. equities market is on track for a negative return in 2015. If this plays out, expect increased calls to shore up pension portfolios and to adjust expected long-term returns downward.

The expected increase in interest rates will also likely dent consumer spending as debt servicing swallows a larger proportion of family budgets. And the higher financing costs will deter larger purchases. Financial officers should anticipate marginally lower sales tax revenues as a result.

LONG TERM RATES CHART

Some Help for ‘Savers’

In addition, the increase in rates could also cool the brisk housing market recovery. As rates rise, housing demand slows as increasing mortgage rates diminish affordability. The housing recovery has been uneven across the country; but since the depth of the housing collapse, prices have rebounded by nearly 30 percent in real terms. Although not quite rivaling the peak of the bubble, these prices are still significantly above long-term trend lines. Property tax revenue forecasts should take these factors into account.

Fortunately, it’s not all negative news. Although the initial impacts from these rate increases may not be welcomed, longer-term a return to normalcy will spur growth by allowing capital to more freely flow to those most adept at creating wealth. As economist David Malpass explains, “Persistent near-zero interest rates punish savers and hurt income growth for average U.S. households. Meanwhile, income inequality worsens as credit flows up the pyramid from middle-class savers earning paltry returns to the upper crust leveraging itself with cheap credit and stock gains.”

As the changes sort out, maintaining a “rainy day fund” with excess cash or short-term fixed investments may be the wisest course of action. This liquidity mitigates the need for painful tax hikes or draconian spending cuts should economic conditions rapidly change as interest rates rise.

OIL POLICY IMPACT CHART

Attachments

Related News

White House launches federal flood standard support website and tool

On April 11, the White House launched a new website and mapping tool to help users with the ongoing implementation of the Federal Flood Risk Management Standard (FFRMS).